.jpg?width=752&name=tablet-pen-portfolio-IS-1171268236%20(1).jpg)

Modern Portfolio Theory (MPT) is the creation of Dr. Harry Markowitz. Markowitz received his Ph.D. in liberal arts from the University of Chicago. His advisers were Milton Friedman and Jacob Marschak.

Markowitz applied risk to stock price analysis, which led to MPT. He published his findings in the Journal of Finance in 1952 (“Portfolio Section”). There were two main points to this work:

- Portfolio Risk

- Diversification

Markowitz’s work was further developed by Dr. William Sharpe (Stanford) and Dr. Merton Miller (Chicago). In 1990, Markowitz, along with Sharpe and Miller, received the Nobel Prize in Economics for his work on the “theory of portfolio choice.”

Modern Portfolio Theory Basics

There are many ways to evaluate risk and return. But if you want to speak one language on this topic, MPT provides that language. MPT is a framework for maximizing expected future returns while minimizing the risk of those returns. This is not to be confused with using MPT as a tactical tool. It is a theory and provides a foundation rather than any specific tool for analysis.

MPT shows how to create a diversified portfolio. There is more to diversifying a portfolio than just buying different types of stocks. Blindly spreading investments out across many holdings is not diversification. Instead, it’s important to combine the right assets with the right weightings to manipulate risk and return in our favor. In addition to evaluating risk and return, MPT includes a third key element: the correlation.

Correlation measures the relation of price movement between two investments (i.e., stocks). If the price of the two stocks moves together, they have a high correlation. If they move in opposite directions, their correlation is negative. Correlation values range from 1 (high correlation) to -1 (low correlation). If there is no correlation, the value is zero.

When diversifying a portfolio, only idiosyncratic risk or the risk associated with each investment can be reduced by combining investments with low correlation to each other. Non-diversifiable risk is called systematic risk. This is a risk that cannot be diversified away.

What exactly is risk? In the context of MPT, risk is variance. Variance is the distance that prices move from a mean. Variance can be measured in standard deviations. An investment with consistent two standard deviation price moves is considered a higher risk than one with one standard deviation move.

High risk is associated with high returns. At the other end of the spectrum is low risk, generating low returns. For example, buying lottery tickets is a high risk but can produce high returns. Not investing and choosing to pile up cash is low risk but very low return (actually, no return). To create a stable (low risk) portfolio is to forego high returns in favor of lower returns

MPT says that if an investment has risk, you don’t need to worry about it. With sufficient diversification, you can eliminate/reduce the risk. (Remember, MPT is a theory, so we can use the word eliminate. In practice, it is better to say reduce instead of eliminate.) If risk is independent (uncorrelated) and returns are uncorrelated with each other, you can make the variance of the average (the variance of the portfolio) go away. Once variance is gone (all prices remain at their mean) and each investment is uncorrelated, there is no risk.

But when risks are correlated, they don’t go away. This is called the law of the average covariance. When diversifying under this scenario, variance doesn’t go to zero; it goes to the average covariance. Think of each investment as risk. When we diversify across a portfolio, we are diversifying risk and in the process, reducing it, assuming those risks are not correlated.

The Efficient Frontier

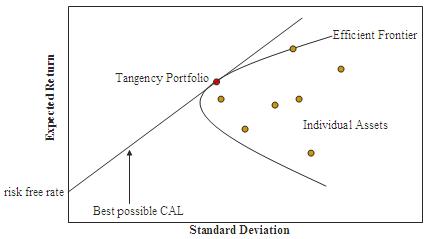

A major component of MPT is the efficient frontier. The efficient frontier provides a graphical representation of MPT concepts. From the graph below, the expected return is plotted on the Y-axis and the standard deviation or variance on the X-axis . The curved line is called the minimum variance frontier. Dots within the curved line are individual assets. Portfolios made up of those assets are located on the curved line.

Source: https://commons.wikimedia.org/wiki/File:Markowitz_frontier.jpg

Starting at the curved line's apex, which is located just below the red dot labeled Tangency Portfolio, and going up, we have the efficient frontier. This is where optimal portfolios are located. Any portfolio below the efficient frontier is sub-optimal. There are no portfolios located above the efficient frontier.

We can see how optimization works by moving left from the red dot. We hit the apex and continue right (and down). Risk is now increasing, but returns are decreasing. If we go back the other way and travel up along the efficient frontier, we are taking on more risk and increasing our return. It is along the efficient frontier that we have the best trade-offs between risk and return.

Finding the most efficient portfolio is called mean variance analysis. Some people just call it portfolio optimization.

While MPT is a theory, it provides practical ideas when thinking about risk and optimization of a portfolio. Going back to the efficient frontier, we can reduce risk by going 100% into bonds (bottom part of the curve and near apex) or maximize returns by going 100% with stocks (far right part of the curve). But at the apex, we may have a 60/40 portfolio consisting of 60% stocks and 40% bonds, providing a fairly balanced and optimized portfolio.

Finding the right portfolio optimization will vary by investor since the portfolio must fit the investor’s investing profile. This can be difficult to do alone. A financial advisor can help investors to find a portfolio that best suits their investment profile.

This material is for general information and educational purposes only. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions.

Diversification does not guarantee a profit or protect against a loss in a declining market. It is a method used to help manage investment risk.

{kind=link}