Investors use various tools to evaluate potential investment opportunities. One of the methods is the internal rate of return or IRR. IRR is useful for comparing different options, especially if they have distinct cash flow patterns and time horizons. In general, a higher IRR anticipates a higher anticipated return.

What Are Good Uses for IRR?

Some investors prefer the IRR to the cap rate because that calculation can't account for changes in cash flow over time, but the IRR formula does. The IRR can also factor in the sales price for an investment along with cash flow before a sale. A critical difference between IRR and another standard valuation tool, ROI, is that the ROI (return on investment) is a function of cost and return, without the time factor that an IRR calculation includes.

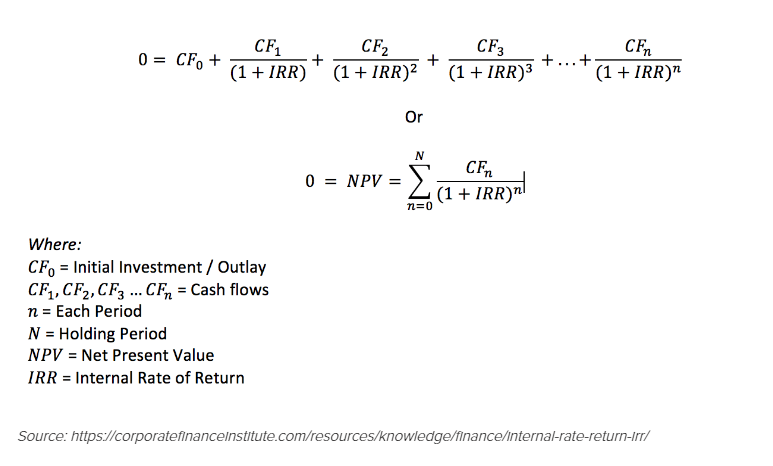

The basic formula for IRR is:

You can also determine the IRR with an Excel spreadsheet, which is usually easier than calculating with a manual formula. The Excel method is beneficial for comparing competing projects. Be aware that if a project has substantial fluctuations in cash flow over time, the IRR may appear deceptively low. Another potential flaw with IRR calculations is for short-term projects—the formula may make the time value of money seem to inflate the return.

Use IRR as One of Several Tools

As mentioned, cap rate and ROI are helpful when evaluating competing projects. There are other considerations that an investor will employ when deciding how to spend available funds. Your priorities are influenced by your goals, investment preferences, and of course, your risk tolerance and risk appetite.

Fund managers sometimes employ IRR when calculating the potential returns for a portfolio, mutual fund, or individual stock. Investors may be considering these advertised numbers compared to potential investments in other assets. In that case, keep in mind that the advertised return assumes that cash dividends are reinvested in the stock or portfolio. That’s potentially a valid choice but can skew the comparison to another type of investment opportunity using the IRR calculation. Further, it excludes other differences between investing in equities and investing in real estate that may impact your overall outcome.

What about Depreciation?

Depreciation is another reason to be careful when using IRR to compare a real estate asset to other investments like stocks. Depreciation is not an expense you pay out directly, but it affects the net income and should be included in the net present value calculation.

Some Investments Have Other Elements to Consider

Formulas are handy, and estimating risk and return is crucial when evaluating competing investments. However, some considerations don't fit neatly in a formula. Tax impact is one element that may influence a choice between competing projects with a similar promise. If you are an investor seeking to defer and potentially reduce payment of capital gains tax on the proceeds of a sale, buying into a QOZ business could make the difference when comparing potential businesses or properties. It's wise to conduct a comprehensive evaluation using analytic tools like the IRR formula and your preferences and individual investing goals.