At Realized, we believe that tax planning in real estate is about seeking opportunities that can help ensure that the amount of money you make remains money you keep. In our second post in this series, we’ll cover an additional tactic to consider when seeking ways to increase your after tax-cash flow: increasing your cost basis.

One way an investor can leverage tax planning to potentially increase the amount of earnings he or she keeps in his or her pocket is depreciation, which we covered in a previous blog. In this post, we’ll discuss the potential benefits of increasing your property’s tax basis.

Tax Shelter Strategy: Increasing Cost Basis

Another strategy to consider, which can be valuable but also comes with more risk, is to increase a property’s tax basis by either borrowing against the property, through a refinance, or taking out additional debt for capital improvement projects.

Here’s a general example of how to increase a property’s tax basis:

$315,000 initial cost basis (purchase price)

+ $50,000 improvements

– $20,000 accumulated depreciation

-------------

$345,000 adjusted basis

This can improve not only your short-term depreciation, but we believe it may also help increase your eventual capital gains.

Taking into account $50,000 in improvements (a basis increase) and $20,000 in depreciation (a decrease), the property’s adjusted basis went up by $30,000 – bringing the overall cost basis up. If, down the line, the property is sold for $400,000, the investor will only owe taxes on a $55,000 gain (vs. $85,000 before the basis adjustment).

Note: This is a simplified example designed to illustrate how increasing your tax basis can lower capital gains, but in reality, there are many factors that contribute to the bottom line.

Another thing to consider here is that while depreciation is a tax shelter that can be used every year the property is owned, selling the property in the future can subject you to depreciation recapture -- up to 25% of the accumulated depreciation.

If you’ve owned a rental property for 20 years and have been taking depreciation every year, that’s a huge chunk of money.

Here’s a look at how increasing cost basis can affect capital gains taxes.

|

Initial cost basis ($85k gain) |

Increased cost basis ($55k gain) |

|

$20,000 depreciation x 25% recapture rate ---------------------------- $5,000 owed $65,000 remaining amount x 15% standard long-term capital gain rate ---------------------------- $9,750 owed Total tax due = $14,750 |

$20,000 depreciation x 25% recapture rate ---------------------------- $5,000 owed $35,000 remaining amount x 15% standard long-term capital gain rate ---------------------------- $5,150 owed Total tax due = $10,150 |

In this case, it’s easy to see how an increased basis helps offset the depreciation recapture -- to the tune of almost $5,000.

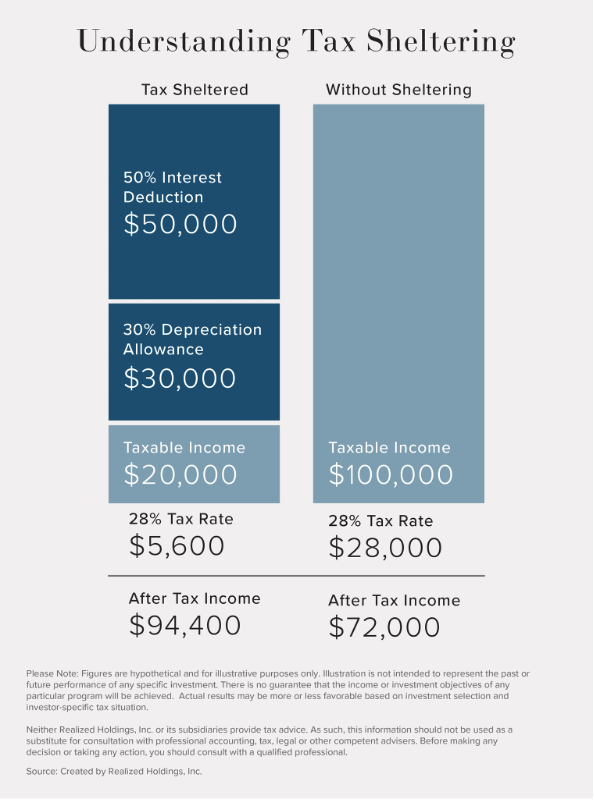

Here’s another look at how income can be sheltered through depreciation. In the tax-sheltered company (on the left), depreciation reduces taxable income from $100,000 to $20,000, which results in a significant difference in after-tax income.

This strategy is designed to give the investor an ability to purchase a higher-value property with a higher net operating income, or NOI.